Getting My Properties for sale in Canada - PrimeLocation To Work

from web site

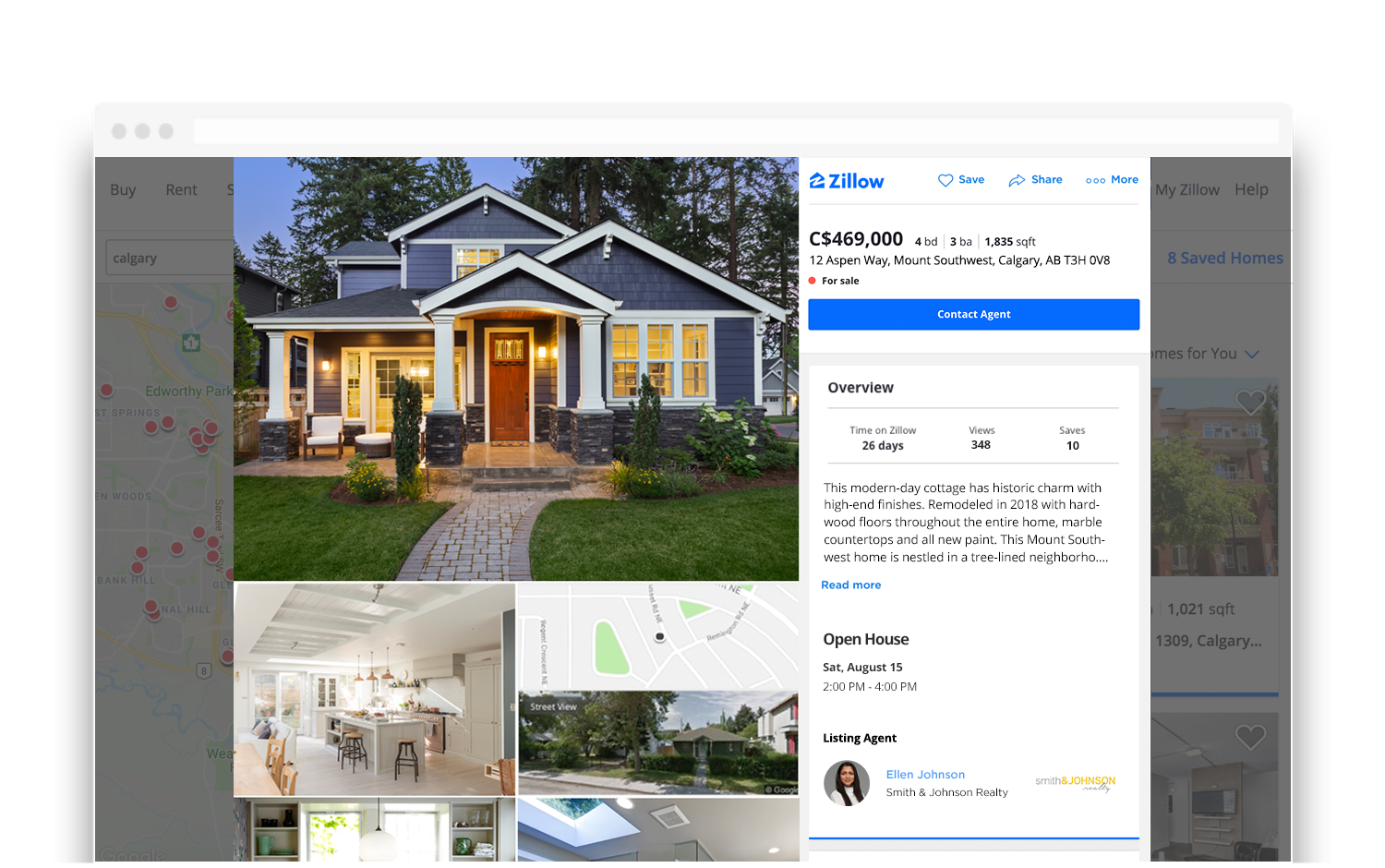

About Properties for Sale - Canada - Cushman & Wakefield

Across the country, new supply was down in about three-quarters of all markets in July. This sufficed to noticeably tighten up the sales-to-new listings ratio despite sales activity likewise slowing on the month. The nationwide sales-to-new listings ratio was 74% in July 2021, up from 69. 9% in June. The long-lasting average for the nationwide sales-to-new listings ratio is 54.

Based upon a contrast of sales-to-new listings ratio with long-lasting averages, the tightening of market conditions in July tipped a small bulk of regional markets back into seller's market territory, reversing the pattern of more balanced markets seen in June. Another piece of proof that conditions might be beginning to support was the number of months of stock.

3 months of inventory on a national basis at the end of July 2021, the same from June. This is exceptionally low still indicative of a strong seller's market at the nationwide level and in the majority of regional markets. The long-term average for this procedure is twice where it stands today. The Aggregate Composite MLS House Price Index (MLS HPI) increased 0.

That deceleration has yet to show up in any visible way on the East Coast where home is fairly more budget friendly. Additionally, a more recent point worth noting (and watching) just in the last month or two has seen costs for particular home key ins specific Ontario markets look like they might be re-accelerating.

Little Known Questions About New Canada, ME Real Estate & Homes for Sale - Redfin.

The non-seasonally adjusted Aggregate Composite MLS HPI was up 22. 2% on a year-over-year basis in July. While still a huge gain, it was, as expected, below the record 24. 4% year-over-year increase in June. Related Source Here -over-year contrast has started to fall is that we are now more than a year removed from when rates really removed in 2015, so in 2015's rate levels are now catching up with this year's, despite the fact that rates are presently still increasing from month to month.