Some Known Facts About Reverse Mortgage Specialist in your area - National Care.

from web site

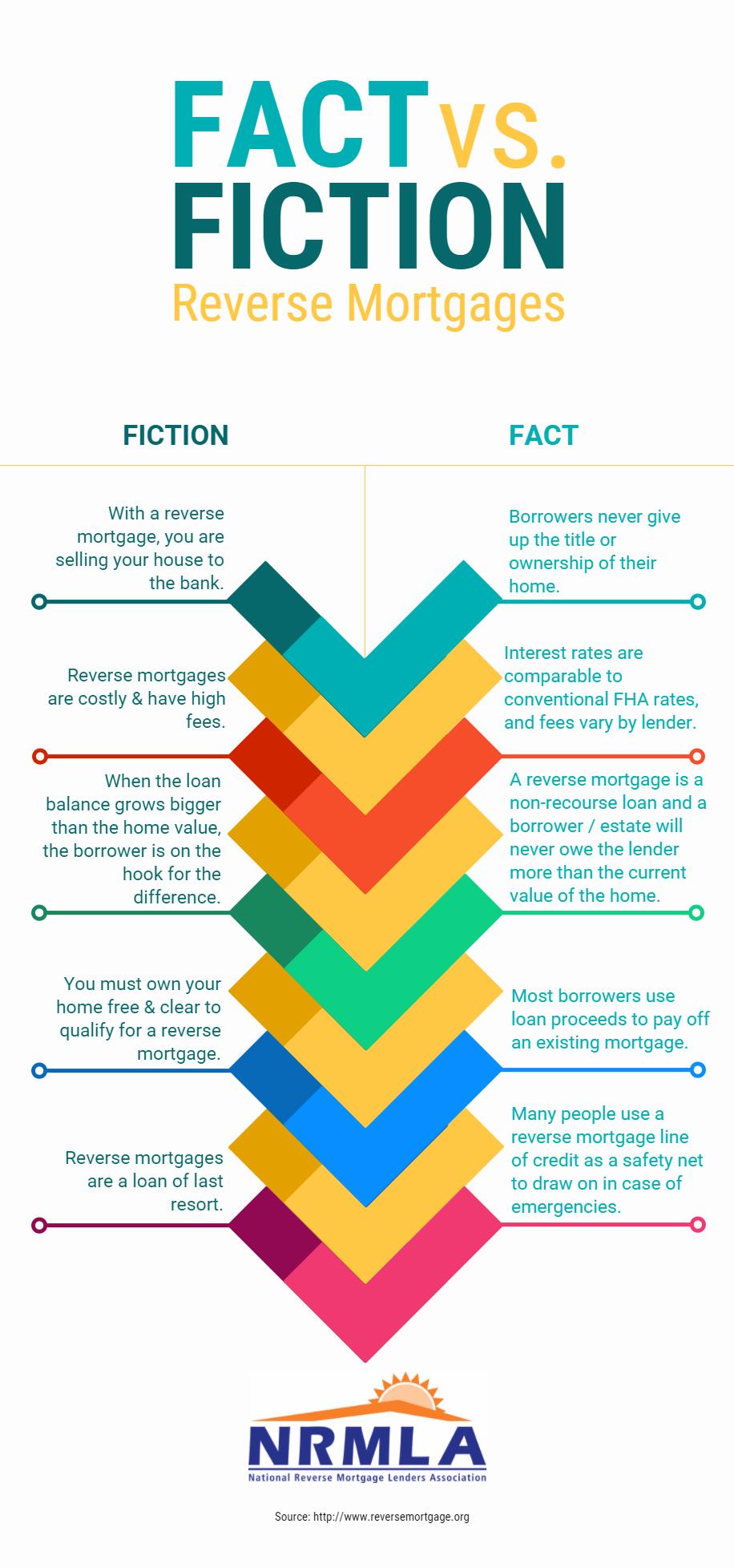

Get This Report on Reverse Mortgages - America First Credit Union

The counselor also should describe the possible alternatives to a HECM like government and non-profit programs, or a single-purpose or proprietary reverse mortgage. The counselor likewise needs to be able to assist you compare the costs of different kinds of reverse home loans and tell you how different payment options, charges, and other expenses affect the overall cost of the loan in time.

Counseling firms usually charge a cost for their services, frequently around $125. This charge can be paid from the loan proceeds, and you can not be turned away if you can't manage the charge. With a HECM, there generally is no specific earnings requirement. Nevertheless, lenders need to perform a financial assessment when choosing whether to authorize and close your loan.

An Unbiased View of Reverse Mortgage - Florida Department of Financial Services

Based on the outcomes, the lending institution could need funds to be set aside from the loan continues to pay things like home taxes, homeowner's insurance coverage, and flood insurance coverage (if relevant). If this is not needed, you still might agree that your loan provider will pay these items. If you have a "set-aside" or you accept have the loan provider make these payments, those quantities will be subtracted from the quantity you get in loan earnings.

The HECM lets you select among several payment options: a single dispensation alternative this is only readily available with a set rate loan, and normally offers less money than other HECM alternatives. a "term" choice fixed month-to-month money advances for a specific time. a "period" option fixed monthly cash loan for as long as you reside in your house.

An Unbiased View of Reverse Mortgage Solutions® (Free Info On Reverse

This alternative restricts the amount of interest troubled your loan, because you owe interest on the credit that you are utilizing. a combination of regular monthly payments and a line of credit. You may be able to alter your payment option for a small charge. Research It Here provide you bigger loan advances at a lower total cost than proprietary loans do.

Taxes and insurance coverage still should be paid on the loan, and your home must be preserved. With HECMs, there is a limit on how much you can get the first year. Your lender will calculate how much you can borrow, based on your age, the rate of interest, the value of your home, and your financial evaluation.