Getting The Home Office: Collect a Tax Windfall - Councilor, Buchanan To Work

from web site

Self Exclusion Program - New Jersey Office of Attorney General Things To Know Before You Buy

Page Last Evaluated or Updated: 24-Jan-2022.

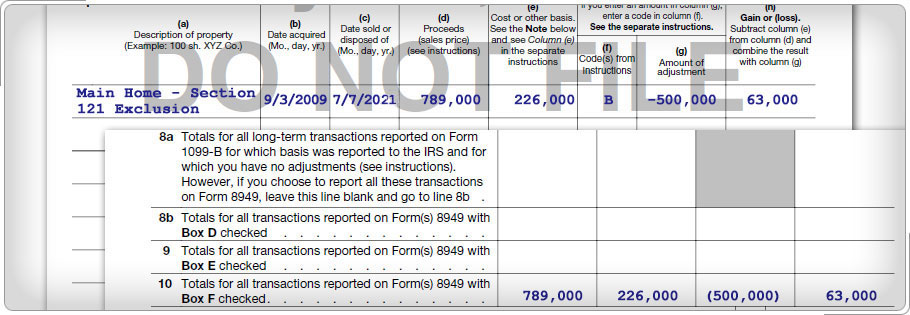

from income under IRC area 121, a taxpayer should own and inhabit the home as a principal house for two of the 5 years right away prior to the sale. Nevertheless, the ownership and tenancy need not be concurrent. The law allows an optimum gain exclusion of $250,000 ($500,000 for particular married taxpayers).

and utilized a home as a principal house during the time his or her deceased spouse utilized the home as a principal house. This rule uses as long as on the day the home is sold the taxpayer's partner is deceased and the taxpayer has actually not remarried. Divorced partners can also gain from the ownership and usage periods of previous partners to satisfy the exemption requirements.

Any post-May 6, 1997 depreciation allowed on the property activates recognition of otherwise excludable gain. exemption every 2 years. However, a taxpayer who disposes of more than one house within 2 years or who otherwise fails to satisfy the requirements, for instance due to a job change or health issue, may get approved for a decreased exclusion quantity.

Getting The The $250,000/$500,000 Home Sale Tax Exclusion - Nolo To Work

FORAN, CERTIFIED PUBLIC ACCOUNTANT, Ph, D, was associate professor of accounting at the University of Michigan at Dearborn. She died in February 2002. View Details J. BRYANT, CPA, JD, Ph, D, is associate professor of accounting at Wichita State University in Kansas. His e-mail address is . or numerous taxpayers their residence is their most important property.

Provisions of the Taxpayer Relief Act of 1997 enable most to exclude from earnings the gain on the sale of a house without even reporting the deal on their tax returns. Proposed regulations clarify the requirements for omitting the gain from income and provide Certified public accountants chances to recommend brand-new tax preparation strategies to their clients.

A taxpayer can declare the complete exemption only when every two years. A reduced exclusion is readily available to anyone who does not satisfy these requirements due to the fact that of a modification in location of work, health or certain unpredicted scenarios. Unlike under former law, the gain on the sale of a home is now completely excluded, instead of deferred, and a taxpayer does not need to purchase a replacement home to leave out the gain.