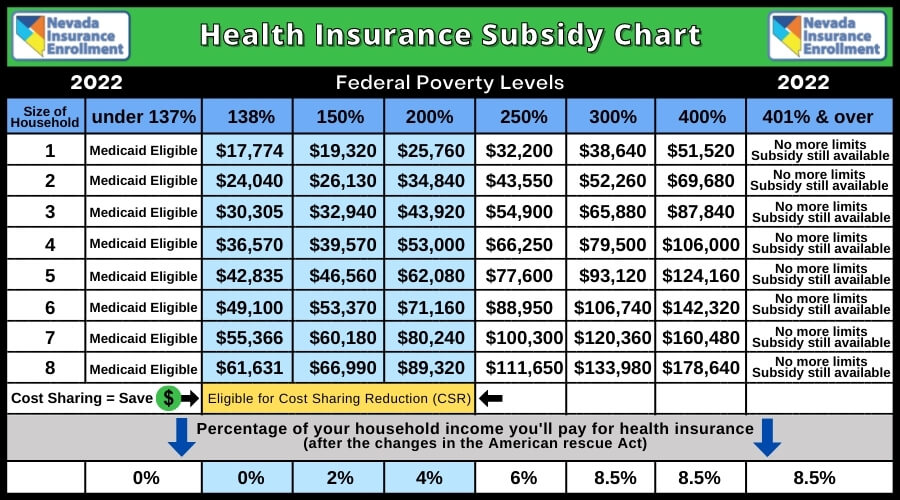

Examine This Report on Covered California Tax Credit

from web site

Not known Incorrect Statements About Get Financial Help - NJ.gov

If you get ill or have an accident, your share of covered medical bills that you will have to pay out-of-pocket will be greater since of the higher expense sharing. Silver strategies are more protective and will have higher regular monthly premiums, however normally have rather lower deductibles and other cost sharing, suggesting you would likely spend less expense when you get treatment.

The Health Insurance Market Calculator shows the cost of silver and bronze strategies in your location. Silver plans are crucial because these are used as a "benchmark" for computing just how much support you are eligible for. Related Source Here shown in the calculator is the second-lowest-cost silver plan in your location.

Bronze plans are the most affordable level of protection that many people are needed to have under the health law. If a Bronze strategy is still unaffordable to you even after monetary assistance, or if you are under the age of 30, you might buy a catastrophic plan. The calculator will inform you when catastrophic protection may be an alternative to you.

Some Known Details About Health Insurance Subsidy (HIS)

To find out more on the difference between bronze and silver plans, see the question on actuarial worth, listed below. With the majority of job-based health insurance, a company pays part of your regular monthly or yearly costs (premiums). In general, individuals who qualify for health insurance through their job are not able to get monetary help through the Marketplaces.

"Minimum worth" indicates your employer strategy pays a minimum of 60% of the total cost of medical services. Your employer can inform you whether the insurance strategy it uses satisfies minimum value. It also can offer you with information to figure out if the plan is considered inexpensive to you. When utilizing the Health Insurance Marketplace Calculator, you can respond to "No" to Concern # 4 if your employer's protection is unaffordable or does not fulfill the minimum value requirement.

Actuarial worth is the percentage of overall covered medical expenditures that are spent for by the insurance provider, on average, for a common population. The greater the actuarial value, the more monetary protection the plan is most likely to provide you when you get ill or require healthcare. For example, if a strategy has an actuarial worth of 70%, then the insurance business will pay about 70% of the total medical expenses for everyone covered by that plan.